Key Takeaways:

- Warsh inherits a Fed caught between Trump's rate-cut demands and 3.8% inflation

- Markets price a 60% chance of a rate hike by year-end, zero chance of a June cut

- His first policy meeting on June 16-17 will set the tone for his tenure

Key Takeaways:

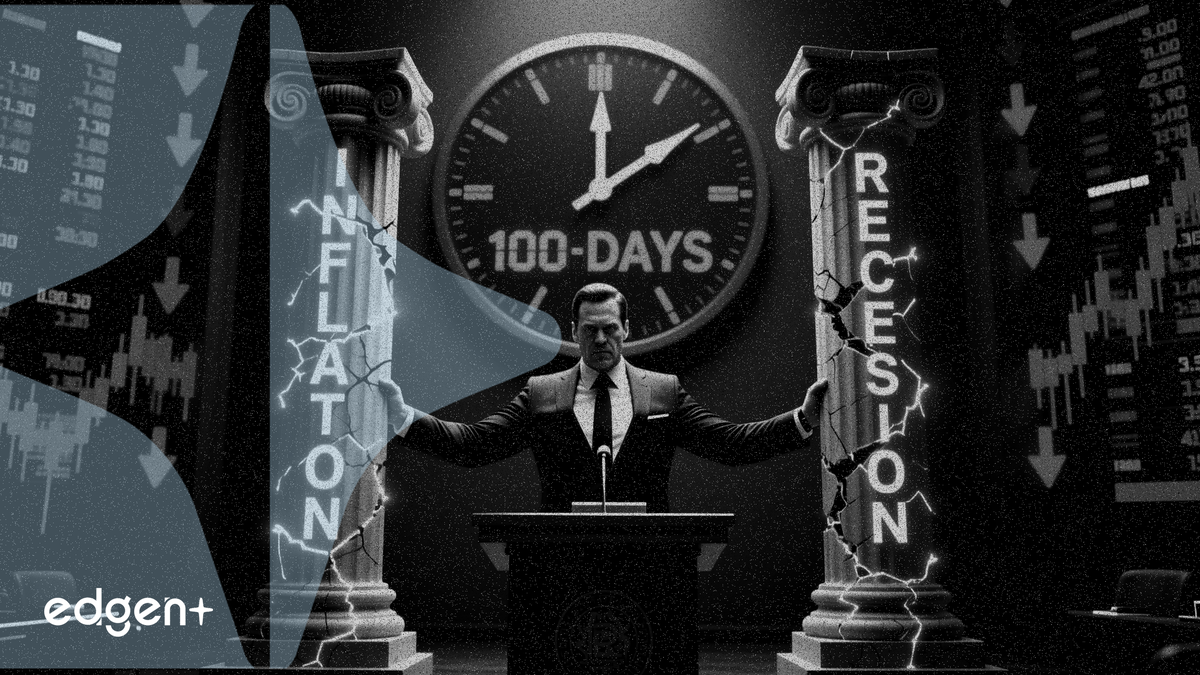

Incoming Federal Reserve Chair Kevin Warsh inherits a central bank caught between President Donald Trump's demand for lower rates and inflation running at 3.8% — a conflict that virtually guarantees a policy crisis within his first three months.

The Fed's next chair faces an impossible arithmetic: Trump wants rate cuts, but inflation at 3.8% and a labor market adding 172,000 jobs a month leave no room for easing. Markets now price a better than 60% chance of a rate hike by year-end, according to CME FedWatch, and zero probability of a cut at the June 16-17 meeting.

"Any hopes of a Fed rate cut have effectively been eliminated with this morning's strong jobs report," said Ronald Temple, chief market strategist at Lazard.

The S&P 500 sank 2.6% Friday in its worst session since October, while the Nasdaq tumbled 4.2% as technology stocks sold off. The 10-year Treasury yield climbed to 4.54% and the 2-year note jumped to 4.16% as traders repriced the rate path. Brent crude settled at $93.09 a barrel, down 2% on the day but still up more than 30% from pre-war levels near $70 before the U.S. conflict with Iran blocked shipments through the Strait of Hormuz.

Warsh's first policy meeting will set the tone for his tenure. If he holds rates steady — the widely expected outcome — he defies Trump. If he signals openness to cuts, he risks unanchoring inflation expectations. Either path carries a measurable market cost.

The Bond Market Is Already Voting

The 2-year Treasury yield surged 12 basis points Friday to 4.16% after the Labor Department report showed 172,000 new nonfarm payrolls in May, well above the roughly 100,000 monthly pace the Atlanta Fed estimates is needed to keep the unemployment rate stable. The 10-year yield at 4.54% reflects term premium for inflation and fiscal risk — not confidence in a soft landing.

The Fed's preferred inflation gauge, the personal consumption expenditures price index, rose 3.8% overall in April, the largest increase in two years. Tariffs and elevated energy costs have broadened price pressures across the economy. The core PCE measure, which excludes food and energy, also ran above the central bank's 2% target.

CME FedWatch data shows zero probability of a rate cut at the June meeting and a better than 60% chance the Fed will need to raise rates before year-end. That pricing predates Warsh's first decision. If the data continues to run hot, he may have no choice but to deliver what Trump does not want.

A Historical Precedent With Key Differences

The last time a Fed chair faced this level of political pressure was the early 1980s, when Paul Volcker raised rates to 20% despite White House objections. The difference: Volcker had inflation above 10% and public support for breaking it. Warsh faces inflation at 3.8% — above target but not crisis-level — and a president who appointed him expecting cooperation.

American and Iranian negotiators reached a tentative ceasefire extension last week, though the agreement has not been finalized. A resolution would ease oil supply constraints and potentially cool headline inflation, giving Warsh more room to maneuver. Without it, Brent crude above $90 keeps upward pressure on gasoline prices and broad inflation measures, forcing the Fed's hand regardless of political considerations.

Warsh's first 100 days will answer a single question: Does the Fed answer to the White House or to its mandate? The market is already pricing the answer.

This article is for informational purposes only and does not constitute investment advice.